Risk Management through CLM

Client Lifecycle Management plays a central role in how financial institutions identify, understand and control risk across client relationships. By coordinating client identity, structure and lifecycle activity, CLM provides the foundation through which institutions manage financial crime risk, regulatory permissions and exposure to complex client networks.

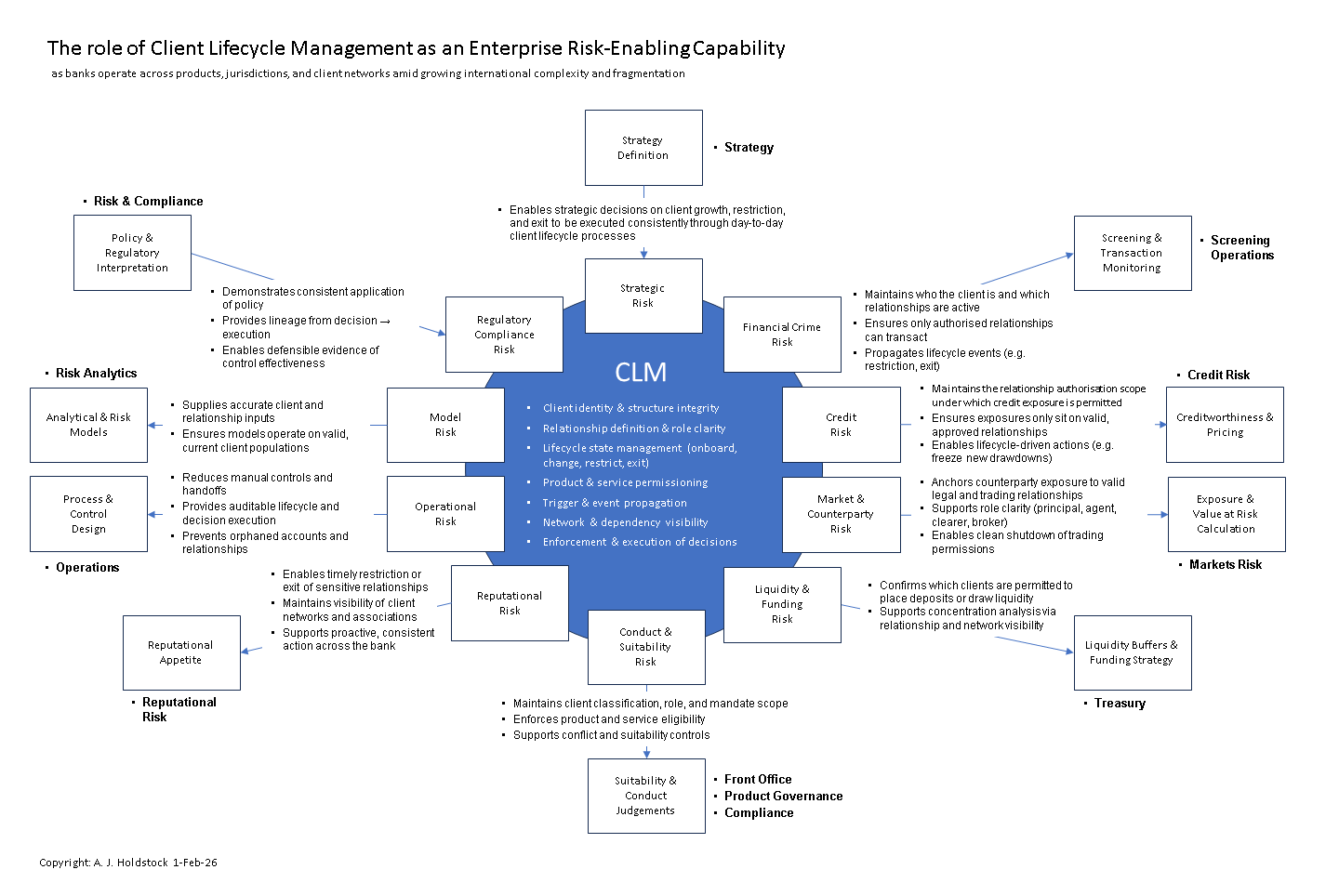

CLM as an enterprise risk-enabling capability

CLM sits at the centre of the bank’s risk and execution model, maintaining the integrity of client relationships and enabling other functions to operate on a trusted, current foundation.

CLM does not assess risk — it ensures that risk decisions can be executed consistently, defensibly, and at scale.

What CLM controls

CLM is responsible for:

Client identity and structural integrity

Relationship definition and role clarity

Lifecycle state management (onboard, change, restrict, exit)

Product and service permissioning

Trigger and event propagation

Network and dependency visibility

Enforcement of lifecycle and risk decisions

Why CLM has become critical for enterprise risk management

Historically, banks could operate without a coherent CLM capability because complexity was lower and control gaps were tolerable.

That is no longer the case.

International fragmentation, heightened geopolitical sensitivity, networked client risk, and regulatory expectations have made relationship control as important as transaction control.

CLM is the missing capability that allows banks to operate safely in this environment.