Why CLM Programmes Fail

and What Successful Firms Do Differently

Client Lifecycle Management programmes have become a major focus for global banks. They are often launched with strong executive sponsorship, large budgets, and ambitious expectations around risk reduction, efficiency, and client experience.

Yet many programmes struggle to deliver their intended outcomes.

In post-implementation reviews the explanation is often framed as a delivery problem — the platform was difficult to implement, the data was messy, or the operating model was not clearly defined. While these factors are real, they usually describe the symptoms of failure rather than its underlying causes.

To understand why CLM programmes fail, it is necessary to look at the issue from several perspectives.

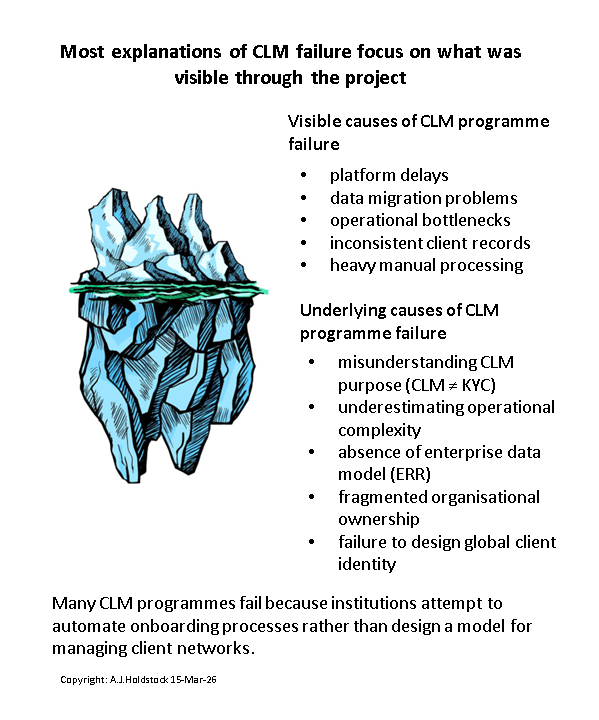

The Visible Causes of Failure

At a practical level, several recurring problems appear across institutions.

Many programmes begin by selecting and deploying a CLM platform before the organisation has fully defined the capability it wants to build. As a result, the programme becomes framed as a technology implementation rather than an enterprise capability transformation.

Other common issues include:

insufficient preparation and standardisation of client and reference data

underestimation of operational complexity across regions and products

fragmented ownership between front office, operations, compliance, risk and technology

excessive customisation of the platform to replicate existing processes

inconsistent regulatory interpretations across jurisdictions

weak engagement from business stakeholders who see CLM as an operational or compliance initiative rather than a core business capability

These challenges frequently appear in programme retrospectives. However, focusing only on these issues risks missing the deeper structural factors that make CLM programmes difficult.

The Deeper Organisational Causes

In many cases the real difficulty is that the organisation has not yet developed a shared understanding of what CLM is meant to be.

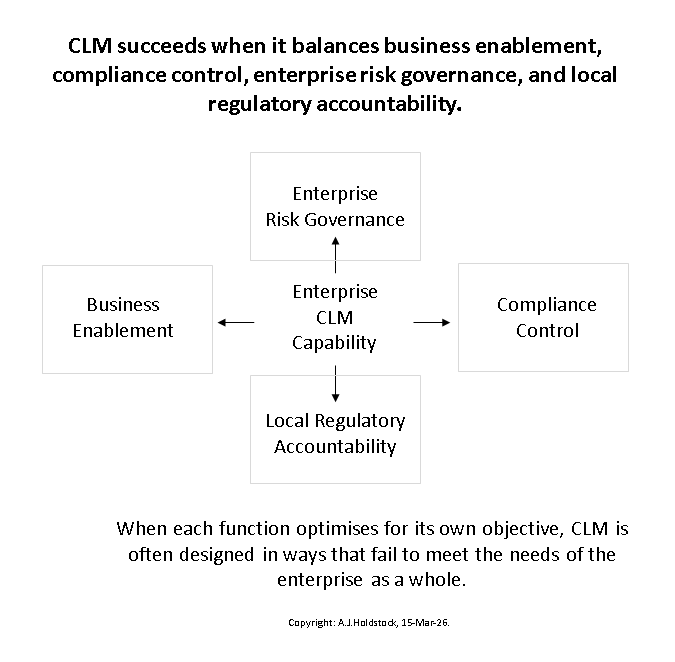

CLM sits at the intersection of client coverage, regulatory compliance, operational processing, and risk management. It touches legal entity structures, booking entities, product relationships, regulatory obligations, and internal governance. As a result, it cannot be treated as a simple workflow or case-management problem.

Programmes become unstable when institutions attempt to implement CLM without first resolving several foundational questions:

Is CLM primarily a risk and control capability, a business enablement capability, or both?

How should responsibility be divided between front office, operations, and second line functions?

How should global standards interact with country-level regulatory requirements?

What is the logical data model that connects clients, legal entities, roles, relationships, products and booking entities?

How should client relationships be governed across a global banking network?

When these questions remain unresolved, the platform implementation becomes the place where organisational disagreements surface. The technology exposes fragmentation that already existed within the institution.

A Familiar Pattern in Large Automation Programmes

There is also a broader historical pattern.

Large enterprise automation programmes have often failed when organisations attempted to automate processes they had not fully understood, standardise models they had not agreed, or industrialise activities they had not yet operationally owned.

CLM transformation programmes can repeat this pattern.

In many banks, CLM as an enterprise capability is still relatively young. Institutions are often attempting to industrialise client lifecycle processes across multiple jurisdictions, regulatory regimes, and business lines at the same time as they are still developing the conceptual and organisational foundations of the capability itself.

The result is predictable: the programme struggles not because the technology is inherently flawed, but because the enterprise capability it is intended to support has not yet been fully defined.

Institutions that succeed with CLM transformation typically approach the problem in a different sequence.

Rather than starting with the platform, they begin with the capability.

This means establishing:

a clear definition of the CLM capability and its objectives

a coherent operating model across business, operations, compliance and risk

a logical data model for clients, entities, roles and relationships

governance structures that align global standards with local regulatory requirements

clear decision rights and accountability across functions.

What successful programmes do differently

Once these foundations are established the technology becomes an enabler rather than a source of friction.

In this sense, the platform becomes an enabler of a defined capability, rather than the mechanism through which the capability is discovered.